# create a data set: x (latent variable) and y (observation)

set.seed(42) # to make it reproducible (lots of random numbers follow)

T <- 50 # number of observations

x <- rep(NA, T) # latent variable

y <- rep(NA, T) # observed values

sx <- 2.2 # standard deviation for x

sy <- 0.3 # standard deviation for y

x[1] <- rnorm(1, 0, 1)

y[1] <- rnorm(1, x[1], sy)

for (t in seq(2, T)) {

x[t] <- rnorm(1, x[t-1], sx)

y[t] <- rnorm(1, x[t], sy)

}

x_true <- x

obs <- yParticle filter using R

particle filter

A simple particle filter in R

The following example was adapted from the post in RPubs.

Simulate the data

Generate \(y_{1:T}\) as a sequence of noisy observations of a latent variable \(x_{1:T}\).

Implement a particle filter (sequential Monte Carlo)

# particle filter -----------------------------------------------------------

T <- length(y) # number of observations

N <- 100 # number of particles

# to store prior distributions for variables correspond to latent variable x

x_prior <- matrix(nrow=N, ncol = T)

x_post <- matrix(nrow=N, ncol = T) # posterior distributions

weights <- matrix(nrow=N, ncol = T) # weights used to draw posterior sample

W <- matrix(nrow = N, ncol = T) # normalized weights

A <- matrix(nrow = N, ncol = T) # indices based on the normalized weights

x_prior[, 1] <- rnorm(N, 0, sx)# initial X from a normal distribution

# calculate weights, normal likelihood

weights[, 1] <- dnorm(obs[1], x_prior[, 1], sy)

W[, 1] <- weights[, 1]/sum(weights[, 1])# normalise weights

# indices based on the weighted resampling with replacement

A[, 1] <- sample(1:N, prob = W[1:N, 1], replace = T)

x_post[, 1] <- x_prior[A[, 1], 1] # posterior distribution using the indices

for (t in seq(2, T)) {

x_prior[, t] <- rnorm(N, x_post[, t-1], sx) # prior x_{t} based on x_{t-1}

weights[, t] <- dnorm(obs[t], x_prior[, t], sy) # calculate weights

W[, t] <- weights[, t]/sum(weights[, t]) # normalise weights

A[, t] <- sample(1:N, prob = W[1:N, t], replace = T) # indices

x_post[, t] <- x_prior[A[, t], t] # posterior samples

}Summarize results

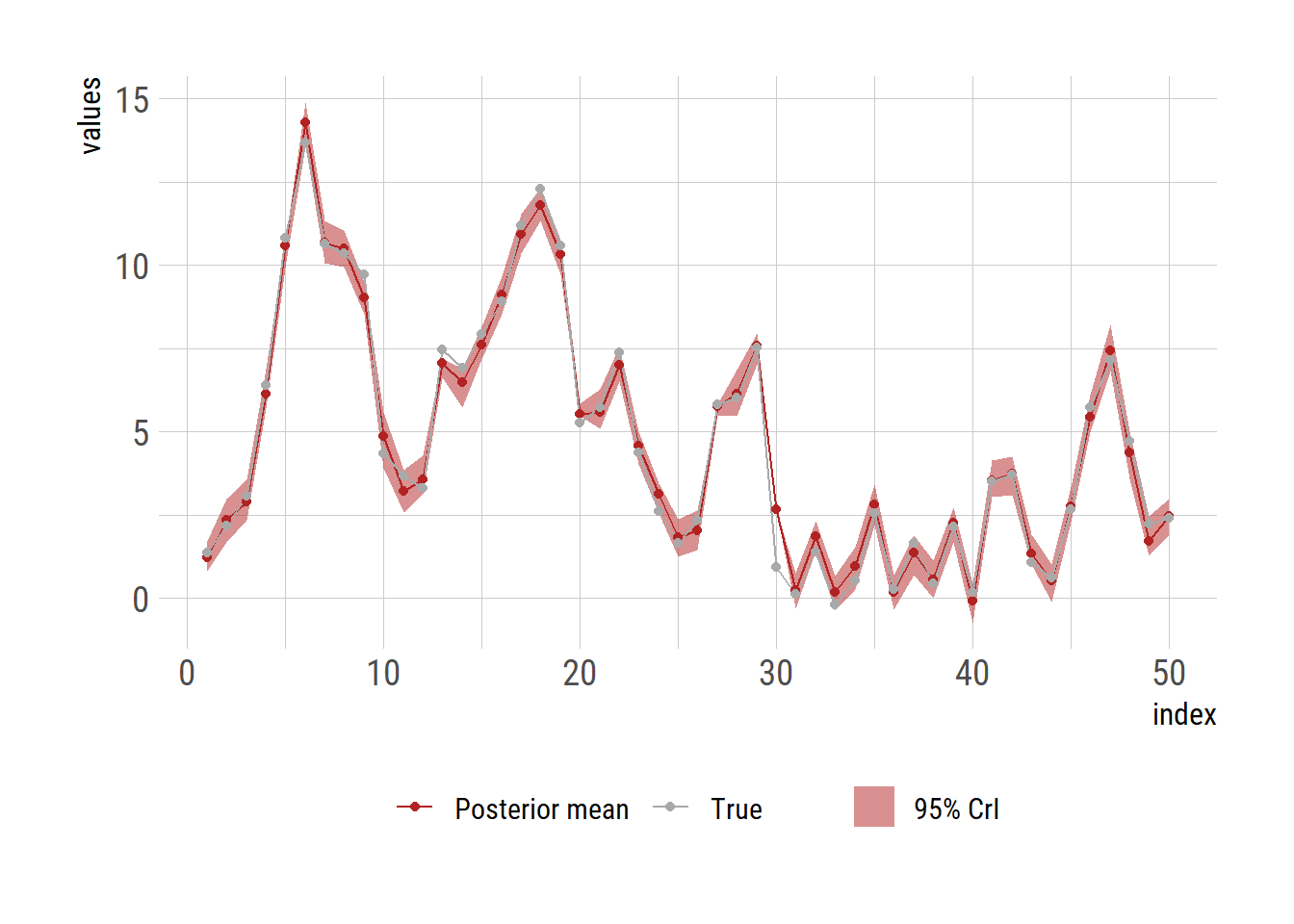

Calculate the mean and 2.5\(^\textrm{th}\) and 97.\(^\textrm{th}\) percentile of the posterior sample as a means to get 95% credible interval.

x_means <- apply(x_post, 2, mean) # posterior mean

x_quantiles <- apply(x_post, 2, function(x) quantile(x, probs = c(0.025, 0.975))) # 95% credible interval

df <- data.frame(t = seq(1, T),

x_mean = x_means,

x_lb = x_quantiles[1, ],

x_ub = x_quantiles[2, ],

x_true = x_true, # latent variables

y = y) # observed valuesPlot the results

library(ggplot2)

extrafont::loadfonts("win", quiet=TRUE)

theme_set(hrbrthemes::theme_ipsum_rc(base_size=14, subtitle_size=16, axis_title_size=12))

ggplot(df, aes(x = t)) +

geom_ribbon(aes(ymin = x_lb, ymax = x_ub, fill="95% CrI"), alpha=0.5) +

geom_line(aes(y=x_mean, color="Posterior mean")) +

geom_line(aes(y=x_true, color="True")) +

geom_point(aes(y=x_mean, color="Posterior mean")) +

geom_point(aes(y=x_true, color="True")) +

labs(y="values", x="index") +

scale_colour_manual("", values=c("Posterior mean"="firebrick",

"True"="darkgrey")) +

scale_fill_manual("", values="firebrick")+

theme(legend.position = "bottom")

# ggsave("particle_filter.png", gg, units="in", width=3.4*2, height=2.7*2)